")

")

Confrontation of the highly strained relations between the United States and Russia over Ukraine has reached its highest peak over the past nine years. While the political passions are focusing inside and around Ukraine, the gas ring around the EU from the north (North Stream-current annual supplies of 36bn cubic meters) and south (South Stream under construction) for the export from the biggest Russian gas producer continues to narrow. On its part, by 2015 the European Union will have completed unification of internal gas networks and power grids, intensified support to constructed re-gasification terminals and switched on a ‘green light’ to new diversification pipeline sources of gas. The European Commission does not accept provision of over 30% supplies by one producer so that someone could dictate his price policy.

Meanwhile, Russia - the holder of the world’s biggest natural gas resources, turned out unprepared to new changes on the global gas market. Russia does not want to lose old positions on the changing markets, giving preference to old rules in a new game, fighting against the rules of the third energy package of the European Commission and the hopelessly outdating form of the take-or-pay contract.

Previous Russian-Ukrainian crises of 2006 and 2009, when gas to European consumers was partially suspended, did not bring anything new to the Russian-Ukrainian relations, but taught Europeans to save gas in their gas reservoirs. The current crisis seems to be the last in its series and most part of the Europeans consider Russia a reliable supplier. At that end of 2015 the EU will receive the first large diversified supplies of liquefied natural gas from the United States, most likely from the Iberian peninsula of Spain. Other capacities will also be launched then.

Changes around the EU were global and multi-vectoral. Over the past five years EU turned from gas importer into exporter. Azerbaijan made its strategic choice between TAP and Nabucco and signed export contracts for 250bn cubic meters with European consumers. Israel found export volumes of natural gas on its shelf and ponders over whether to direct gas from the Leviathan field (nearly 500 bn cubic meters of extractable resources) to Europe or to South Asia. Turkey lobbies connection of gas capacities of Iraq, Iran and possibly Israel to the Azerbaijani-Turkish exportation system. This will help Turkey form a specific South Henry Hub for 500-million European market.

In addition, several Australian projects on liquefied natural gas are expected to be launched by 2016-2017, which will raise the capacities for production of liquefied natural gas in the country from 20 mln tonnes in 2011 to 125 mln tonnes in 2017, as well as three plants to liquefy pipeline American gas of a total volume of 50-55mln tonnes of liquefied natural gas.

The South Stream gas pipeline is not a political priority for Europe as Russia insists, since even if the project might be different from Nord Stream but the supplier is still the same-Gazprom, which does not seek to accept provisions of a third energy package as a main cause for its restructure.

The statement came from chairman of the European Commission Jose Manuel Barroso, foreign media report.

EU’s current energy strategy envisages fight against dependence on foreign suppliers through shifting to spot prices (compared with take-or-pay contracts on which Gazprom insists) and creation of a single system of power supply (at least 10% of electricity generated in the EU must be commonly available). “Not a single country must remain power-isolated by 2015”, the official communiqué of the European Council reads. However, the demands in energy sources of a third part of the EU member-states, including Finland, Poland and Baltic states, are still met almost through Russian supplies. Russia accounts for nearly a third of gas consumed in the EU.

Import of shale gas from the United States may help change the situation. The statement came from British Premier David Cameron who urged during the EU summit to include energy into the sphere of negotiations on creation of the free trade area between the EU and the United States, which was predicted on the pages of Caspian Energy in November 2012.

The European Council plans to consider alternative ways of replacing gas consumption, including energy from renewable sources and conventional ones-nuclear power and coal. Production within EU member-states currently meets almost a third part of the demand, however, according to the forecasts of the European Commission and the International Energy Agency, this indicator will inevitably decline. “If we do not take active steps today, Russian oil and gas supplies will make up to 80% of overall consumption in EU in ten years”, President of the European Council Herman Van Rompuy warned the summit participants.

Stake bigger than gas

The growing demand for gas in EU is primarily dictated by a decline in production (30% of consumption) in the EU countries.

In particular, gas extraction on the continental shelf of Great Britain is dropped by almost 25 bn cubic meters per year. According to representative of the German association of power economy Roland Schmidt, Germany will reduce gas extraction on its territory in the upcoming decades, compensating for this with foreign power supplies. Germany’s current consumption is covered by 34% by Russia, 31% by Norway, 19% by Netherlands, while its own sources cover demand for gas by 12%.

Hopes for Norway are also not too high. In the short-term perspective we can raise gas extraction but not too significantly”, Norwegian Oil and Energy Minister Tord Lien said in an interview to Handelsblatt. He reminded that country’s gas extraction will be raised to 130bn cubic meters by 2020. This indicator is to make 110 bn cubic meters in 2013. A greater part of gas is directed to EU states via pipelines.

Reuters refers to the words by the Norwegian minister who said Europe may raise purchase of liquefied gas. Capacities on receipt of liquefied gas and its transportation to consumers have been expanded dramatically lately. This will expand the share of such suppliers as the United States or African countries.

The first supplies of liquefied natural gas from the United States to the European market are expected by no earlier than the end of 2015. US Energy Secretary Ernest Monis said in an interview to a Czech television.

“If we take the current cost of gas on the US market, add expenses on gas liquefaction, transportation, and, probably, construction of any gas pipeline, the price-if this gas is supplied to the Czech Republic-will be almost the same as you are paying now. But this will be a different source of supplies and this will have a pressure on other gas suppliers”, Monis said. However, according to him, in making decisions on gas export, great importance will be dedicated to geopolitical criteria. “Though the US demand for oil and gas is growing dramatically, the energy security of our friends and allies coincides with the interests of our security. And diversification of power supplies is its main tool here”, the minister said.

Despite this, the main hopes of Europeans will be bound to the Southern gas corridor, US Secretary of State John Kerry said. It is noteworthy that the secretary of state of the country which is preparing to the large-scale export of its liquefied gas to the world markets urges to prioritize the question of ‘how to receive more natural gas by the Southern Gas corridor transporting it from Azerbaijan to Turkey and further to Europe.

“We believe that there are no grounds for panic”, Saine Berger, Press Secretary of the European Commissioner for energy told Deutsche Welle. She said Europe expects Russia to further fulfill its commitments on gas supplies. The same expectation refers to the transit commitments of Ukraine”, Berger added.

In case this happens and Europe faces the threat of failure in gas supplies via Ukraine, EU will be prepared to this better than before in previous years. The heating season has passed, winter in Europe was warm and there are big volumes of gas reserves in reservoirs. ‘Today there are nearly 36bn cubic meters of gas in EU’s gas reservoirs, which means they are almost half-filled”, the spokeswoman for the European Energy Commissioner said. This is approximately the same volume which is imported from Russia by Germany-EU’s largest economy. According to Ministry for Economy, Germany’s gas reservoirs account for 13bn cubic meters. “This indicator is above average for this season”, sources in the ministry said emphasizing that ‘Germany is well prepared to possible problems with the gas transit via Ukraine”.

John Kerry said this during the 2 April EU-US session on energy issues in Brussels. He said there are other opportunities including construction of LNG-terminals in Europe, as well as pipelines to supply gas to consumers. This statement probably means that domestic market (see Caspian Energy #8, 2013) is a top priority for the US administration, since cheap energy sources are among the main stimulus of competitive economy and further industrial growth of the United States. In addition, the main export of the United States will likely be oriented to the Asian-Pacific countries, where gas has been traditionally more expensive. Therefore, supplies to Europe via the Atlantic will have rather a psychological impact on the market in terms of support to European partners.

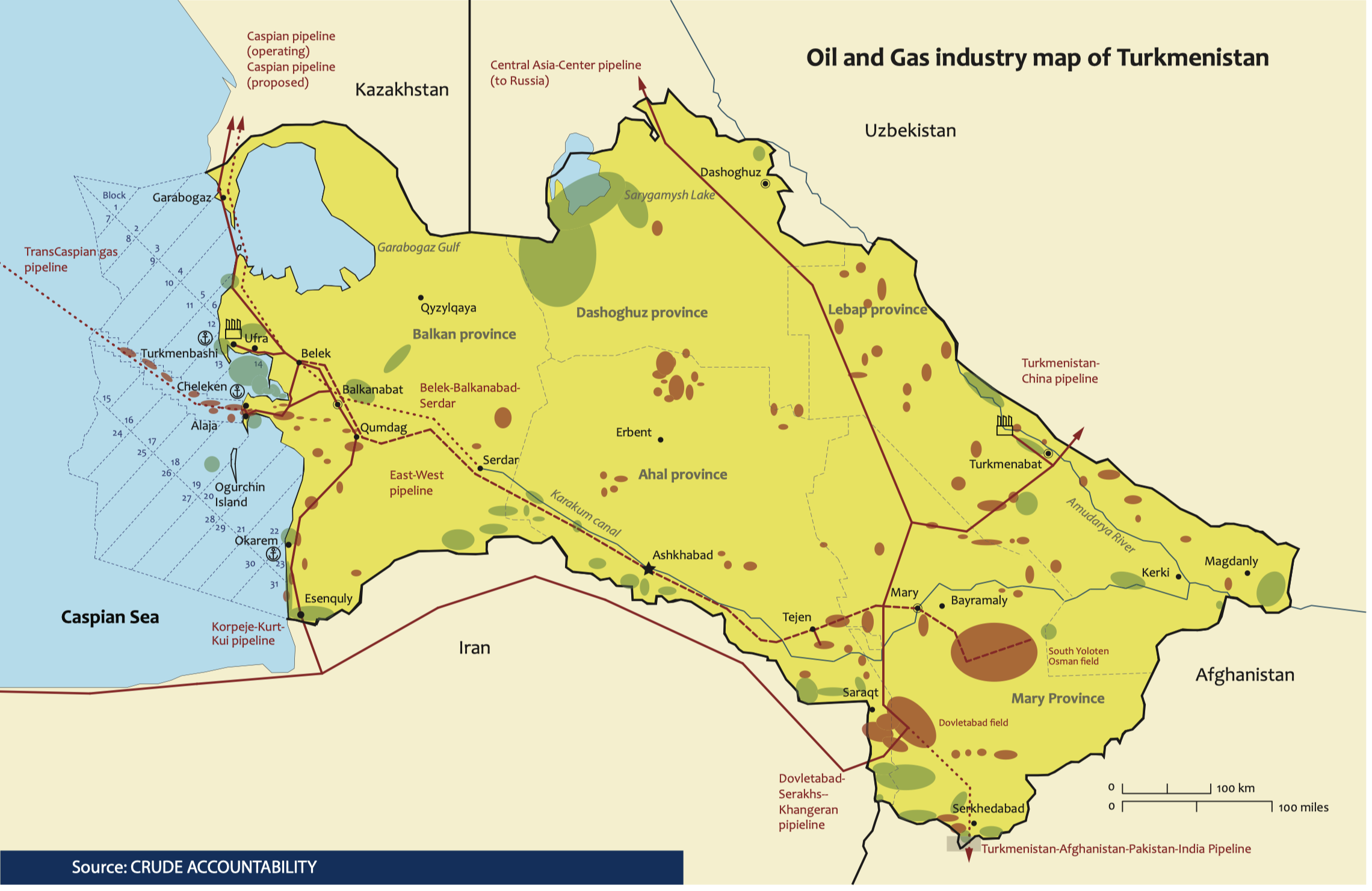

The main attention will be paid to the Caspian natural gas of Azerbaijan and possibly of Turkmenistan which by 2015 will have completed construction of the East-West connecting pipeline designed for main fields.

Turkmen gas for Nabucco?

If the matter concerns about the consolidation of the Southern Corridor, accelerated development of nearly 3 trillion cubic meters of extractable reserves for Azerbaijan is the issue of the next 5-7 years with further increase of 30 bn cubic meters export limit after 2020. In case of Turkmenistan, this is primarily the achievement of political and intergovernmental agreements with the EU and Azerbaijan, ensuring state guarantees of supplies of definite volumes of natural gas, attracting investors and construction of respective infrastructure. Depending on possible volume of supplies, initially they are likely not to exceed 10 bn, it may be necessary to raise the project capacity of both Trans Anatolian Pipeline and launch new export capacities in Europe, since the Trans Adriatic export gas pipeline from Greece to Italy-TAP is intended for Azerbaijani gas. Probably, the matter will be about restoration of Nabucco or development of its new version, for example, the Trans-Danube project from Romania to Austria, supported by Romania and the European Commission.

According to the Minister of Oil and Gas Industry and Mineral Resources of Turkmenistan who spoke in Berlin last year, there is a plan to extract 230bn cubic meters a year and export 180 bn cubic meters annually by 2030.

Hydrocarbon reserves of the Caspian Turkmen shelf are estimated at 2bn tonnes of oil and 6.5 trl cubic meters of gas. Several contractual areas, located at medium and deep water areas were put on an international tender.

Nearly three years ago Turkmennebit started to assimilate the deepwater part of the sea.

Turkmenistan’s largest fields are concentrated in the Mary province, east of the country. The overall reserves of Galkinish with surrounding fields were estimated by local geologists and British GCA at a range of 26.2 trl cubic meters.

Considering the above mentioned, intensive striving of consumers to diversify sources of supplies will inevitably lead to creation of new biggest hubs in the South: in Turkey and south-western EU (in the Pyrenees) using the example of Henry Hub in Louisiana or northern NBP (largest of EU’s seven continental hubs) in Great Britain. And as a result they may lead to the conclusion of a definite part of contracts on the basis of spot deals. This will happen by 2020 and the current so-called Ukrainian spring has become the main catalyzer of the formation of free southern gas market.