")

")

Caspian Energy (CE): How efficient was the 2013 year for the ECO Trade and Development Bank (ETDB)? What are the Bank’s plans for the coming 2014?

Hossein Ghazavi, President, ECO Trade and Development Bank: First of all, I would like to provide brief information about the ETDB and its main mission. The Bank has been functioning since 2008 and has a vision to become the financial pillar of economic cooperation among ECO member states fostering sustainable economic development and integration. It is structured and operating as a regional Multilateral Development Bank (MDB) similar to WB, ADB, IDB, EBRD, BSTDB, etc. The policies, rules and regulations adopted in this respect are all aligned with the practices of other MDBs and the needs of member states. Within this framework, the Bank provides financial and technical support to private and public sector for implementation of development projects, expansion of intra-regional trade and accelerating economic development of ECO member states.

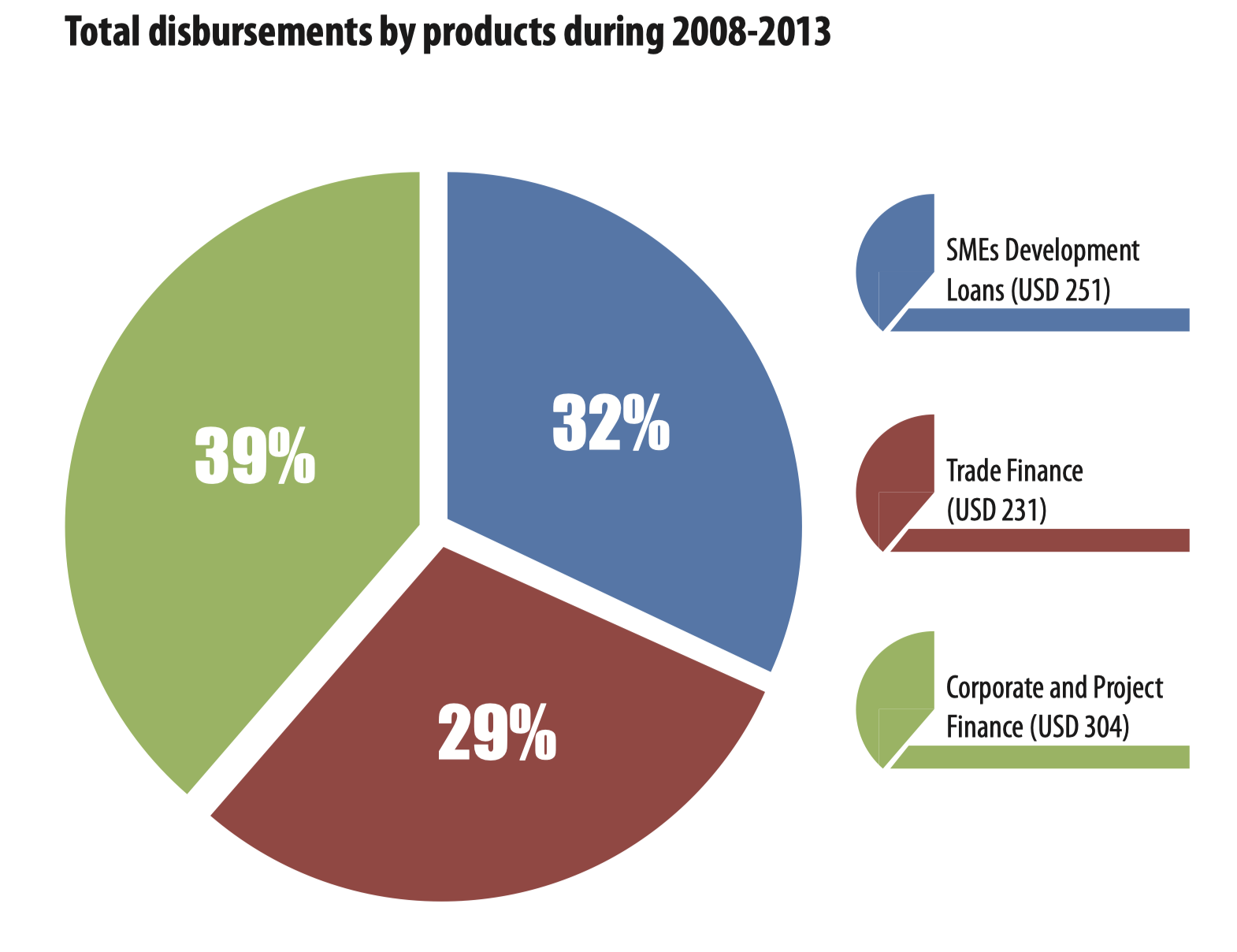

During the past several years the Bank has achieved considerable milestones, even though it is the youngest regional MDB in the world. It has been able to build up an efficient organizational structure and established fundamental internal regulatory framework to improve its development effectiveness, governance and additionality. In this respect, accountability, transparency and adherence to sound banking principles have always been placed at the core of our operations. Within this short yet continuous business span, the Bank has been able to introduce a range of medium-to-long term products and services for enhancing trade, development of SMEs, meeting the financing and technical assistance needs of corporates and projects in the member counties. In this connection, the total amount of loans disbursed to various operations in the member states amounted to USD 786 million by the end of November 2013. The Bank has been posting a positive net income without having any non-performing loan in its well diversified portfolio.

The Bank has been receiving overwhelming support from its shareholders and business partners. During the coming years we would certainly continue to focus on improving our services and achieving more shares in mobilizing development finance to the region. In a nutshell, despite persisting global economic challenges, the Bank currently finds itself in the very special position of being a reliable development partner in the region. Building on our knowledge and expertise we would further capitalize on our specific roles and contribute sustainable development of our member states. In line with strategic objectives set out in its establishment agreement and Business Plan for 2013-2017, the Bank would advance its vision over the coming period.

CE: World’s leading economies are in the process of post-crisis development. How do system banking crises affect the activities of the ETDB?

Hossein Ghazavi: We have been observing some encouraging improvements in the global economy but we also know that sustainable growth is still prone to many interrelated risks. The current global economic landscape can best be summed up as one of cautious optimism. There is still no effective multilateral surveillance to bring discipline and responsible behavior for better crisis management. In addition, the problem of moral hazard has no perfect solution, but requires further credible common mechanism to limit it. The extraordinary, unconventional monetary policy measures taken by major advanced economies which cannot be sustained forever need to return to more normal levels gradually as the economic growth and stability restored.

However, no one wants this process to happen in a disorderly manner. Nevertheless, this normalization process would have negative spillover effects on some developing, economies including ECO countries. It is, therefore, important for ECO countries to be vigilant and consolidate gains and further build on domestic and regional forces of growth. If I may comment, the overall policy responses of ECO member states to the global economic crisis so far have been relatively successful. The region showed considerable strength in the post global crisis years, particularly in 2010 and 2011. The nominal GDP of the region touched another peak of USD 1.95 trillion in 2012 and is likely to exceed USD 2 trillion for the first time over the next years. During the post crisis-era, building on sound macroeconomic policies, industrial diversification, stronger financial systems, buffers in foreign reserves, enhancing competitiveness and efficiency would put regional economies in a far better position.

I would like to underline that the ability of the financial sector to efficiently play its intermediary function is fundamental for a sustainable economic growth in the region. The global financial crisis did not have significant affect on the region’s financial sector because of sound financial regulation and supervision, as well as adequate macro-prudential measures. Banks in the region particularly have strengthened their balance sheets and business practices, making them more resilient to external shocks. However, this resilience was the result not only of the prudent business approach, but also sectors limited global financial interconnection, including conservative innovation and competition status.

Overall, the financial sector in the region has been developing significantly. The region is also making progress in developing domestic capital markets and non-banking financial services such as leasing, factoring and microfinance, etc. The sector is introducing new products, services and intensifying supervision and competition measures. The major players in the sector are making significant efforts to mobilize long-term resources to finance the massive investment requirements. Therefore, securing a stable, solid, financial sector of a reasonable size relative to regional GDP is a key concern. Within this framework, we support development of financial institutions and promote financial system’s capabilities to play its role in sustainable development. A large share of our operations in the financial sector is represented by trade finance and SME credit lines extended through financial intermediaries. We are making efforts to extend our partner network with relevant financial institutions in the member states and started to work with leasing companies, Islamic banking and microfinance institutions as well. We will continue to support development of financial institutions in the region with an aim to improve access to financial services for corporations, SMEs, and households, particularly the poor, in the region’s growing and diversifying economies.

CE: What peculiar features does the ECO Bank have unlike world’s similar structures? Do you plan to admit new members?

Hossein Ghazavi: I would like to emphasize that it is important for ECO countries to promote higher levels of economic and social integration in order to realize potentials of the region. Within this perspective, the role of the ETDB becomes more evident in promoting sustainable development, cooperation, mobilizing resources and generating benefits for its members. To this end, I am very happy to inform that the ETDB has positioned itself as a viable development institution to contribute advancing regional goals and aspirations. The most compelling comparative advantage of the ETDB is clearly its regional ownership. We put utmost effort to deliver funds for priority development needs of member states on competitive terms with minimum delays. In this respect, through a mutually agreed policy dialogue with relevant national authorities, we formulate country strategies for each member country, including economic, thematic and sector policy analyses in order to address the targeted investment needs. We have to ensure the optimum contribution of our operations to the development of member states. Our institution serves as a vital source of knowledge and expertise on growth and development in the region. Combined with its strong local presence in the region, the Bank is better placed to understand development challenges and opportunities. The targeted operations of the Bank also play an important role in reducing the risk perceptions about our member states individually and about the region as a whole while boosting the confidence of investors. Capitalizing on our specific and localized roles we act as a reliable business partner for global institutions that are investing or interested to operate in the region. In this respect, further strengthening our mutual cooperation with peer institutions remains among our top priorities. We are collaborating on issues of similar interest, identify joint business opportunities, and share know-how and best practice experiences. I am confident that in the coming years we would accelerate concluding cooperation agreements and initiate exemplary co-financing projects/operations in our common member countries.

With regard to expansion of Bank‘s membership base, I hold the belief that eventually all the ECO member states would join the Bank. In this regard, we continue to pursue a comprehensive program to encourage the other ECO member states to become a member of the Bank. Indeed, their membership is undoubtedly a valuable source of potency for us to further expand operations with full regional ownership. Azerbaijan became the fourth member of the Bank and Afghanistan is processing to finalize the remaining membership procedures. The other five ECO member states are expected to accelerate the process of their membership in the coming years. We are making necessary arrangements ready to carry forward successful operations in the new member states as well. At this point I would like to emphasize that as a reliable brand name of the region in development finance we stand ready to continue our assistance to all ECO member states for the achievement of their development objectives. Therefore, with strong support of regional countries, we look forward to play more positive and effective role in the years beyond.

CE: What is the credit portfolio of the Bank now? What is its structure?

Hossein Ghazavi: Diversification of its loan portfolio remains one of the important business development guidelines of the Bank. As I have stated the Bank has been able to achieve sound financial ratios without registering any non-performing loan in its well-diversified portfolio across countries and sectors. We provide short-to-long term loans to both private and state owned entities. Since development of private sector can play a crucial role in expanding trade and investment links between ECO member states, we encourage more active public-private cooperation. The overall distribution of the Bank‘s intervention reflects the priorities and opportunities available from time to time in each member state. Besides attaining optimum risk/return ratio, development and integration impact, in particular, tends to preclude a preferential factor in allocation Bank‘s resources to different projects and operations. It is pertinent to mention that the Bank does not intend to maximize profits in the course of its activities, but seeks to at least recover its operating cost and the cost of capital and maintain healthy financial ratios. The Bank rather focuses on financing development programs and projects at reasonable costs with favorable repayment conditions.

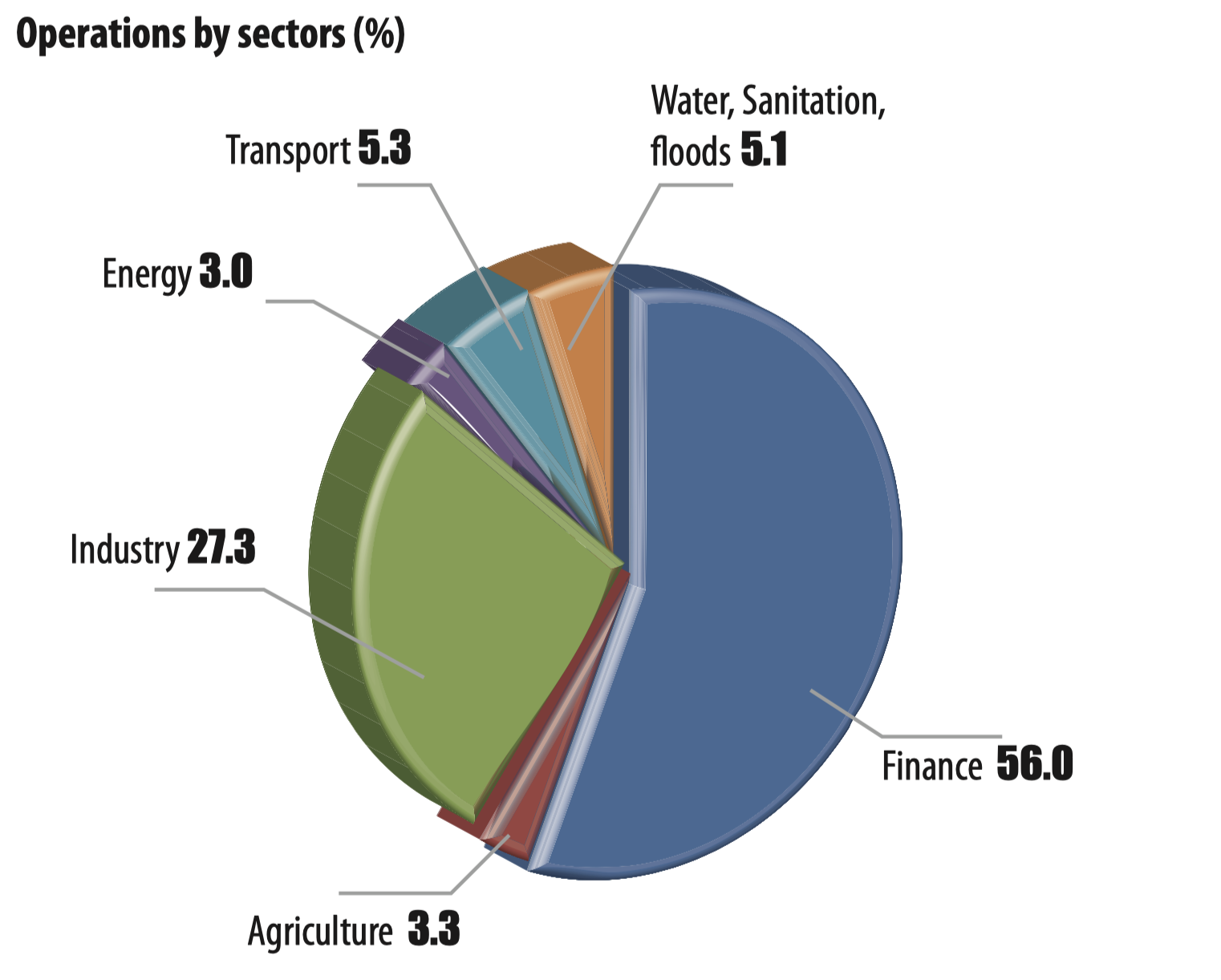

Overall, the Bank takes lending decisions solely on the merits of projects, programs, or other transactions proposed and tailor borrowing in line with the best opportunities available in the capital markets. The financial structure of a project/transaction, financial strength of the sponsors, technology, quality of the collateral, tenor, and sector are also important determinants in this regard. We specifically consider the relevancy and impact of our operations to the development objectives of the member countries. In this context, the portfolio of the Bank is diversified towards sectors such as manufacturing, finance, trade, infrastructure, energy, transportation and agriculture. Meanwhile, the Bank ensure firm adherence to enterprise-wide risk management approach to mitigate concentration risk and strictly avoid practices which are detrimental to its institutional reputation and financial position.

CE: The ECO as a regional organization intends to promote trade among member countries. Will the Bank take part in these plans?

Hossein Ghazavi: The ECO region is full of bright cooperation prospects. The common ties of history, geography, faith, culture and converging interests in diverse fields contribute most meaningfully to the uplift of this region and its people. Since its establishment in 1985, the ECO has developed into a thriving regional organization. The member states are cooperating on development of several projects/agreements in priority sectors such as trade, transport, industry, agriculture, energy and communication as well as culture, education and banking. People in the region are already feeling the positive outcome of economic integration, and governments of ECO member states realize that these projects must be continued.

I am very pleased to state that regional cooperation efforts are deepening in terms of increased trade and investment flows, commercial ties as well as development of regional transport infrastructure. When we look at the trade figures, in 2012, the total external trade of the ECO member states exceeded USD 900 billion with about 10 percent intra-regional trade record. These are promising developments, but we need to further build on them and harness ECO’s full potential to bring tangible benefits to the people of the region. When we compare the ECO to other regional organizations like ASEAN, where the volume of intra-regional trade is 24%, or the EU where the figure is almost 70%, we find that we have a lot of work to do to fill this gap. The intra-trade ratio of 20 percent can be immediately achieved, if regional economies make efforts to fully implement the agreed measures. I believe that the region has the potential to transform into a prosperous trading bloc through stimulating and promoting industrial growth, reducing tariff and non-tariff barriers and become a factor of global peace, stability and prosperity. In this respect, the regional preferential trade agreement namely, ECO Trade Agreement (ECOTA), which is under implementation process, will eventually lower tariffs in the region. Furthermore, the objective of enhancing intra-regional trade requires the presence of a well-functioning system of transport in the region. To this end, implementation of the Transit Transport Framework Agreement (TTFA) and realization of infrastructure projects in main transport-logistics corridors will be instrumental. Moreover we need to overcome supply-side challenges and promote trade facilitation measures. Of course, we should ensure that the private sector feels seriously part and parcel of this process and should be fully involved in shaping trade policies and trade negotiations. It is also relevant to remark that four members of the ECO are members for the World Trade Organization (WTO)-Turkey, Kyrgyzstan, Pakistan and Tajikistan. Since regional and multilateral trade liberalization efforts go in parallel, the accession of other ECO member states to WTO should also be supported.

Therefore, with the right policies in place, the ECO region shall capitalize on its potentials and recognize the trade as the engine of economic growth. Within this framework, it has been the strategic objective of the Bank to improve and enhance the level of intra-trade among ECO member states. Since the start of our operations, the Bank has adopted a very prudent trade finance program. We are supporting funding needs of traders directly and through credit lines extended to the financial intermediaries such as commercial banks, leasing companies, export credit agencies in the member countries. The Bank offers a number of services, including loans, issuing guarantees, discounting, forfaiting, buyer’s credit, which all are designed to meet all different requirements in trade finance. Today, several financial institutions in the member states are benefiting from our trade finance facility. At the same time the Bank has started to introduce some other products in order to increase its role in enhancing trade finance transactions. I would like to underline that the Bank will continue to enter into new agreements and introduce mechanism in order to achieve more share in financing and supporting the regional trade.

Thank you for the interview