")

")

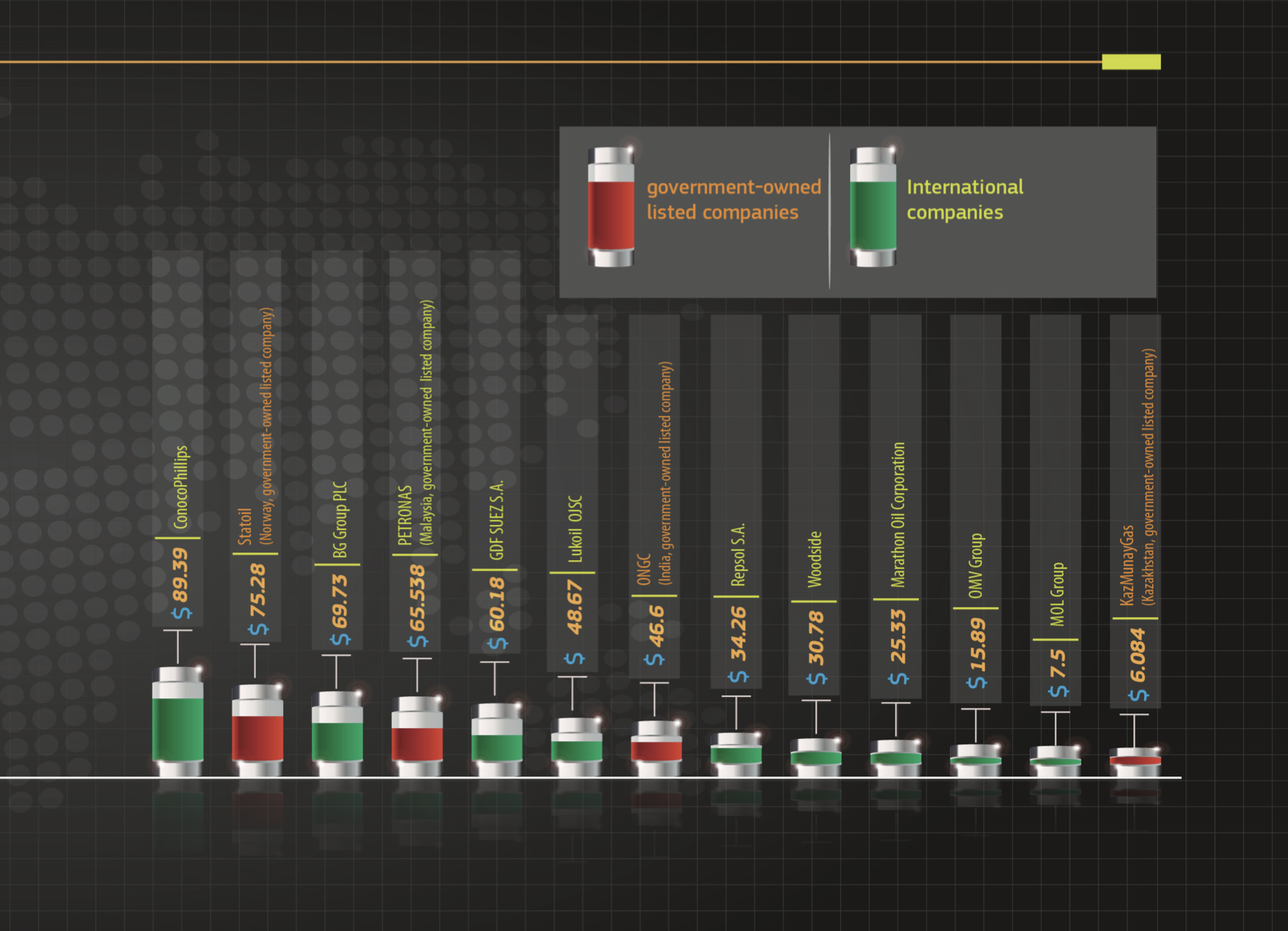

According to ‘Caspian Energy-2013 Rating’, in the expiring year seven sisters-majors ExxonMobil, BP, Shell, Chevron, Total, ConocoPhillips, and Eni had even more opportunities to establish kin relations with government-owned listed companies involved in the international capital-related operations including CNOOC, Petrobras, PetroChina, Sinopec, Statoil, Rosneft, KazMunaiGas, Gazprom and ONGC. Five-year influencing of globalization on all segments of the energy market still continued. It is well observed in the rapprochement of the North American and European markets with the signing of the Comprehensive Economic and Trade Agreement between Canada and the EU, and the similar transaction is currently in process between the USA and the EU. Besides, the Canadian-European agreements are considered as a general rehearsal of the upcoming rapprochement of the two largest world markets (USA and the EU).

The recovering US economy offers hand to the European market that needs a footing in the form of cheap energy carriers to encourage expansion of production, establish a post-crisis operation of the integrating banking system of the EU and resolve the social crisis. Cheap energy carriers in the United States have already enabled to make production by 15% cheaper than in the EU and by only 8% more expensive than in China and this process is still continued.

This year China has remained the main source of capital, continuing to buy up treasury bonds of the growing ceiling of the national debt of the USA. It also one of the ways to draw Chinese financing for development of resources in the neighboring countries - Russia, Turkmenistan and Kazakhstan, which then are to go to the People’s Republic of China. By 2017 China shall become world’s largest oil importer, leaving behind the present leader - the United States. China is raising import of crude hydrocarbons while the US reducing. It will inevitably affect both the oil price in these countries and the scheme of transport flows of raw materials. According to experts’ estimations, spending of China on oil import will have made $500 billion by 2020, while similar expenses of the USA are to decrease to $160 billion by this time. Thus, China’s oil import will grow by 360%, while US import will go down by 32%.

The economy of China will grow by only 7.7% this year instead of expected 10%. The Chinese government stakes on development of the domestic market, reducing an export component. Chinese companies continue aggressive purchasing of assets worldwide starting from Canada to Kazakhstan. State-owned companies are becoming more and more active in the international cooperation with majors and vice versa. The steadily high corridor of oil prices throughout the year has encouraged growth of market capitalization of oil-gas companies and accordingly investments into exploration and mainly in the gas infrastructure in different oil and gas provinces worldwide – from the Norwegian Arctic to the coast of Latin America.

Caspian events in 2013

The main events of the 2013 year in the energy sector are related to exploration of the Arctic reserves, the potential of the LNG market and nonconventional energy resources.

According to the annual market researches performed by the analytical group of Caspian Energy among experts involved in implementation of large upstream projects, they have pointed out to the two main events in the Caspian that will promote further integration of Caspian energy resources into the world markets.

The contracts of Shah Deniz Consortium (with Statoil as a commercial operator) on gas sales to the European market for the sum of $200 billion for the period of 20 years have become an important event of the year in Azerbaijan.

In the opinion of experts, the launch of the largest oil project: Kashagan, Aktoty, Kayran area (10-13 billion barrels of recoverable reserves) on the Caspian shelf of Kazakhstan in September of the current year was the main event of the year in the Caspian even despite the following emergency suspension of production because of the gas leakage. Production is scheduled to be resumed in the end of 2013.

As regards the Russian sector, on October 1, 2013 Prime Minster of the Russian Federation Dmitry Medvedev signed the executive order, granting the license to Caspian Oil Company for production on the West Rakushechnoye field in the Caspian Sea discovered by Caspian Oil Company in 2008. Earlier, the company had the license only for geological exploration of the site of subsoil resources. Oil production on Y.Korchagin field is currently in process.

Reserves of hydrocarbons on the field exceed 270 million barrels of oil equivalent. The maximum level of production will reach 2.5 million tons of oil and 1 billion cubic meters of gas per annum.

Dragon Oil PLC has informed about the increase of oil production in the third quarter of this year up to 74,300 barrels a day on the contract territory Cheleken located in eastern part of the Absheron chain in the Caspian Sea off Turkmenistan. All offshore oil of Turkmen is exported via the Baku-Tbilisi-Ceyhan pipeline. In 2013 Turkmenistan will also ramp up oil production to 75-80 billion cubic meters per annum thanks to the commissioning of the giant Galkynysh gas field and raise supplies up to 40 billion cubic meters of gas for China, to 10-11 billion cubic meters for Russia and to 14 billion cubic meters for Iran.

The following stage of the field development will enable to raise exports to China by 25 billion cubic meters per annum. In 2012 Turkmenistan supplied the People’s Republic of China with about 30 billion cubic meters of gas (13 billion cubic meters from the contractual territory Bagtyyarlyk, where Chinese CNPC is producing on the basis of PSA provisions, and 17 billion cubic meters from the left bank of the Amu Darya River).

Iran, continuing the process of talks with world’s six leading economies to negotiate mitigation of the sanctions for its oil export, has made it clear that it is ready to demonstrate legislative flexibility by offering, for the first time in its history, India to sign the first PSA contract on Farsi gas field.

World Rating

Upstream

Norway, the main gas supplier to the European market, expressed readiness for commencing drilling of wells in the former disputed zone of the Barents Sea. For the first time since 1994 Norway is preparing to open a new oil-gas bearing province, 1.9 bln of oil equivalent is at stake.

The Brazilian oil company Petroleo Brasileiro SA (Petrobras) announced about start of five year investments worth $236.7 bln into development of large oil fields discovered over the past decade. It will help to maintain oil production on “aging” fields located in the basin of Campos which accounts for up to 85% of oil produced in Brazil. Petrobras sold a minority stake in 5 exploration blocks (north-east of Brazil) to the British BP. The blocks are located in the basin of Potiguar (equatorial zone of Brazil).

ConocoPhillips and China National Offshore Oil Corp. (CNOOC) received permit from the authorities of the People’s Republic of China to resume production of 40,000 barrels per day on the offshore block Penglai 19 (Bohai gulf).

LNG

Declining trade of LNG was the milestone event of the expiring year. This segment of the world market has been in decline since 2012 (a 2% decline down to 232 mln tons) and that has been associated not with the reduction of demand but mainly with subjective factors that are to promote the deficiency growth and push the demand upwards in future.

In the Asian-Pacific region it is a delay of implementation of the Australian LNG projects due to the rising costs. In particular, big mining projects which attract the most qualified personnel are competing with Gorgon and 6 more under-construction LNG plants in Australia. The Australian oil-gas corporation Woodside Petroleum postponed its plans on realization of the Browse LNG project in the western part of Australia. Browse was expected to become the largest project of Woodside. Though, the corporation’s plan to erect capacities at James Price cape was criticized by ecologists and the local population;

In Europe it is non-fulfillment of contract obligations by Nigeria in regard to the European suppliers as well as shortage of gas storages and LNG terminals. Despite the decline of demand, a certain window of LNG deficiency is observed in Europe due to the EU’s policy, aimed at reduction of coal consumption, and due to incomplete supplies from the African countries. Spain will become the EU’s leader on LNG import (16 bcm) this year. The country is re-exporting part of the volumes to the Latin-American countries and neighboring Portugal.

The LNG infrastructure is developing very intensively in North America. USA is preparing to export over 100 bcm of LNG by 2016. Russia is accelerating the realization of its three northern LNG projects in accordance with the global demand. The Russian LNG is going to cover the rapidly growing Asian market.

The US Department of Energy has this year granted the fourth license for sale of the liquefied natural gas (LNG) to the Dominion Resources Company from the terminal located in the state of Maryland. Head-quartered in the city of Richmond (the state of Virginia), Dominion Resources will be able to supply during 20 years up to 21 mln cubic meters of LNG per day to Japan and other countries that have no free-trade agreement signed with USA. USA permitted to export a total of 58 bcm of liquefied natural gas.

The Malaysian company Petronas (Petroliam Nasional) intends to invest $34.96 bln in LNG production projects in Canada.

The government of Canada has given a final permission to the Anglo-Dutch Royal Dutch Shell to export liquefied natural gas from the planned LNG-plant of the company in the Pacific coast of the British Columbia province. This permission will let export up to 670 mln tons of LNG for 25-year period. The license was given to the consortium consisting of Royal Dutch Shell, Japanese Mitsubishi Corp, Chinese PetroChina and South Korean Korea Gas Corp.

It is the third similar license given in Canada.

The largest Russian independent gas producer NOVATEK, the CNPC Company and the Consortium of the Chinese Banks signed a memorandum about financing of the Yamal LNG project aimed at construction of the liquefied natural gas production plant in Yamal. Novatek and Chinese CNPC have earlier signed the agreement on the sales and purchase of 20% of the Yamal LNG project. The deal is planned to be sealed till December 1, 2013. The Chinese party undertook an obligation to lend assistance in attraction of external financing to the project from the Chinese financial institutes.

The agreement also envisages signing of a long-term contract with NOVATEK for LNG supply to China (at least 3 mln tons of LNG per year).

Gazprom is to commission two LNG plants in 2018. The first line of the Vladivostok-LNG project with the minimum capacity of 15 mln tons per year will be launched in 2018.

Nonconventional resources

Nonconventional resources continue a victorious procession. The boom of shale resources started in 2010 in the United States slowly, but consistently expands towards China, the European countries, Saudi Arabia, Azerbaijan and Russia.

According to the data of the US Department of Energy, recoverable shale oil reserves are as 75 billion barrels in Russia, 58 billion barrels in the US and 32 billion barrels in China.

Total shale oil reserves worldwide comprise 345 billion barrels. It is approximately the one tenth of all recoverable oil reserves across the globe.

China, Argentina and Algeria are the top three leaders in terms of recoverable shale gas resources. Total global shale gas reserves are estimated at 145.98 trillion cubic metres, accounting for 32% of all global recoverable crude hydrocarbons.

Poland has been the first in Europe to start production of shale gas in 2013. Lane Energy Poland company controlled by ConocoPhilips is producing about 8,000 cubic metres of gas a day on the test well in the north of the country near Lembork city.

Great Britain intends to considerably ramp up production of shale gas in coming years to maintain competitiveness of the national economy. According to the statements of the government, the United Kingdom is rich with as much as 37 trillion cubic metres of shale gas. Taking into consideration that usually only around 10% of all reserves turn to be recoverable, this volume still will be enough to meet all energy demands of the national economy for 100 years.

The government of Germany has announced the draft law on production of shale gas that could protect the German citizens from negative effects of hydraulic fracturing technology. The draft introduces environmental “preventers”, forbidding hydraulic fracturing on nature protection territories and near wells with drilling water. It covers 14% of the territory of Germany. In addition, environmental impact assessment is obligatory conducted for each project.

The Chinese government approved a production sharing agreement of Royal Dutch Shell PLC and the Chinese National Petroleum Corporation (CNPC) for exploration of shale gas reserves in China in early 2013. The matter concerns joint exploration, development and production of shale gas from the Fushun-Yongchuan block in the Province of Sichuan.

Shale gas exploration of CNPC-Shell covers 3,500 km.

Earlier the Chinese officials stated country’s intention to produce 6,500 million cubic meters of shale gas per annum by 2015, OGJ informs. The American Hess Corp signed a PSA with CNPC for development of shale gas in the Province of Sichuan. The Malang block in the northeast of China occupies 800 square kilometers.

Saudi Arabia is planning to drill seven exploration wells for share gas by the end of the year. At present Saudi Aramco is exploring shale gas formations in the northwest of Saudi Arabia.

Baker Hughes has estimated that Saudi Arabia is just behind China, US, Argentina and Mexico in terms of recoverable reserves of share gas available (17 trillion cubic metres).

In Azerbaijan ExxonMobil and Total express interest to development of combustible gases fields. Azerbaijan is rich with as many as 50 fields of combustible gases in Gobustan, Lower Kura lowland and other regions of the country.

In Russia there is the Bazhenov field, one of world’s largest shale oil formations. According to preliminary estimates, the formation can possess 100 billion barrels of oil, which is five times more than the reserves in Northern Dakota. All largest Russian oil and gas companies, including Gazprom, Rosneft, Surgutneftegaz and Lukoil, are engaged in development of this field, using the equipment and technologies from Texas and Northern Dakota. The Russian government introduces tax privileges for companies, since without such privileges expensive production from shale formations would have become unprofitable.

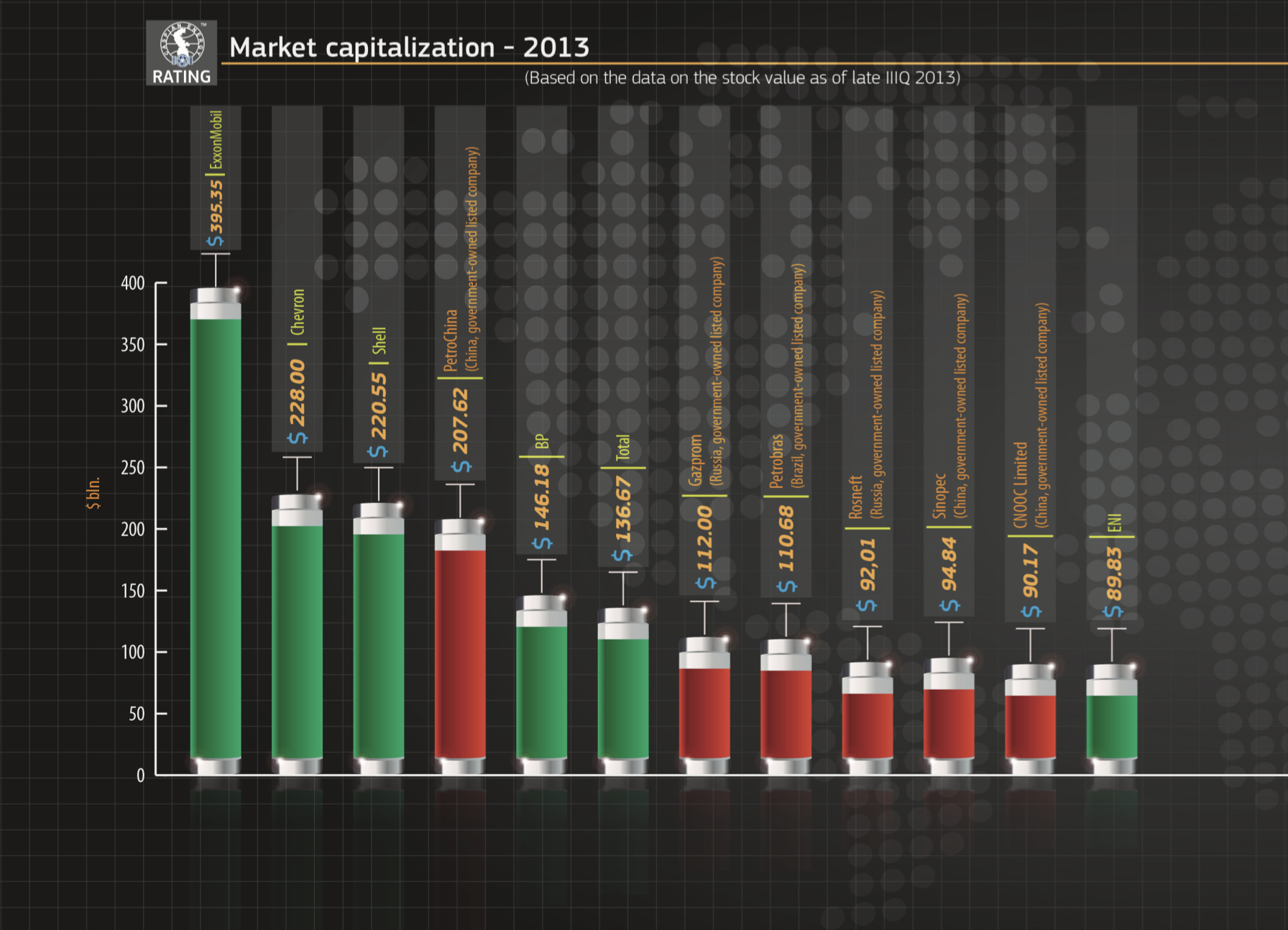

Market capitalization - 2013

(Based on the data on the stock value as of late IIIQ 2013)

In late 2013 the market capitalization rating for world’s largest oil-gas companies has three majors on the top, mainly Exxon, Chevron and Shell. This year the Chinese company PetroChina has topped the list of government-owned public majors with the 4th position in the ranking. The list of world’s top 10 most expensive companies included also two Russian government-owned companies as well as Petrobras (Brazil).

So, the world’s first top 10 most expensive oil-gas companies in ‘Caspian Energy - 2013 Ranking’ is equally shared by both private and government-owned majors. The competition for assets of government-owned companies, technologies and better management is becoming tougher and tougher. Analysts foresee a continued volatility of boundary of private and government-owned assets in the oil-gas sector.