")

")

Having overcome all obstacles on its way, in September Azerbaijan signed new contracts with the European companies 12 years later the first export agreement with Turkey reached in 2001. These contracts envisage supply of 250 bcm worth $200 bln within 25 years.

Long-term agreements on sale of gas from Shah Deniz Stage II to Europe have been signed with the following companies: Axpo Trading AG, Bulgargaz EAD, DEPA Public Gas Corporation of Greece S.A., Enel Trade SpA, E.ON Global Commodities SE, Gas Natural Aprovisionamientos SDG S.A., GDF SUEZ S.A., Hera Trading srl and Shell Energy Europe Limited.

It is a big breakthrough of Azerbaijan towards the world market. The country’s role as an influential world energy player and partner for other Caspian states is strengthened and expanded. As for even quite relative and average calculations as well as statements made by SOCAR officials, it turns out that Azerbaijan and its partners will gain a total of $800 (approx $22.8 mmBtu or $76, 2 MWh) per 1000 cubic meters within a 25-year period.

The distinguishing feature of the contracts is that Shah Deniz gas aims at the EU countries where gas prices have traditionally been high and demonstrating the “ceiling value” over EUR 32 MWh (400 EUR per 1000 cubic meters) for the past years, in countries like Greece, Italy and Bulgaria.

On the one hand, a wide list of the European partners of SOCAR points out to high liquidity of Azerbaijani gas in Europe, on the other hand it points out to high profitability of Caspian gas production projects. And all of this happens despite the costs faced due to the almost 10-year delay of Shah Deniz project implementation.

On the one hand, without going into details of math calculation of risk ratio, indicators of expenditures and internal rate of the Caspian mega-project profitability, and on the other hand, considering the European climate requirements forming the main trend of the European gas prices in future, it is noteworthy that the previous Shah Deniz export contract envisaged purchase of 79.7 bcm (during 2007-2018).

According to the gas purchase agreements signed between Azerbaijan and Turkey on March 12 in Ankara, Turkey has been annually purchasing 6-7 bcm of Azeri gas since 2007 and will be buying this volume till 2017. The Azerbaijani-Turkish agreement “On supply of Azeri gas to the Turkish Republic during 2004-2018” signed in Ankara on March 12 envisaged commencement of “blue fuel” export from Baku to Erzurum in 2003. As for the document the Turkish side is to purchase 79.7 bcm of gas from Azerbaijan during 15 years. According to the agreement, gas extracted from Shah Deniz field will flow to Turkey in the volume of 2 bcm, 3bcm, 5 bcm and 6.6 bcm in 2004, 2005, 2006 and 2007-2018 respectively.

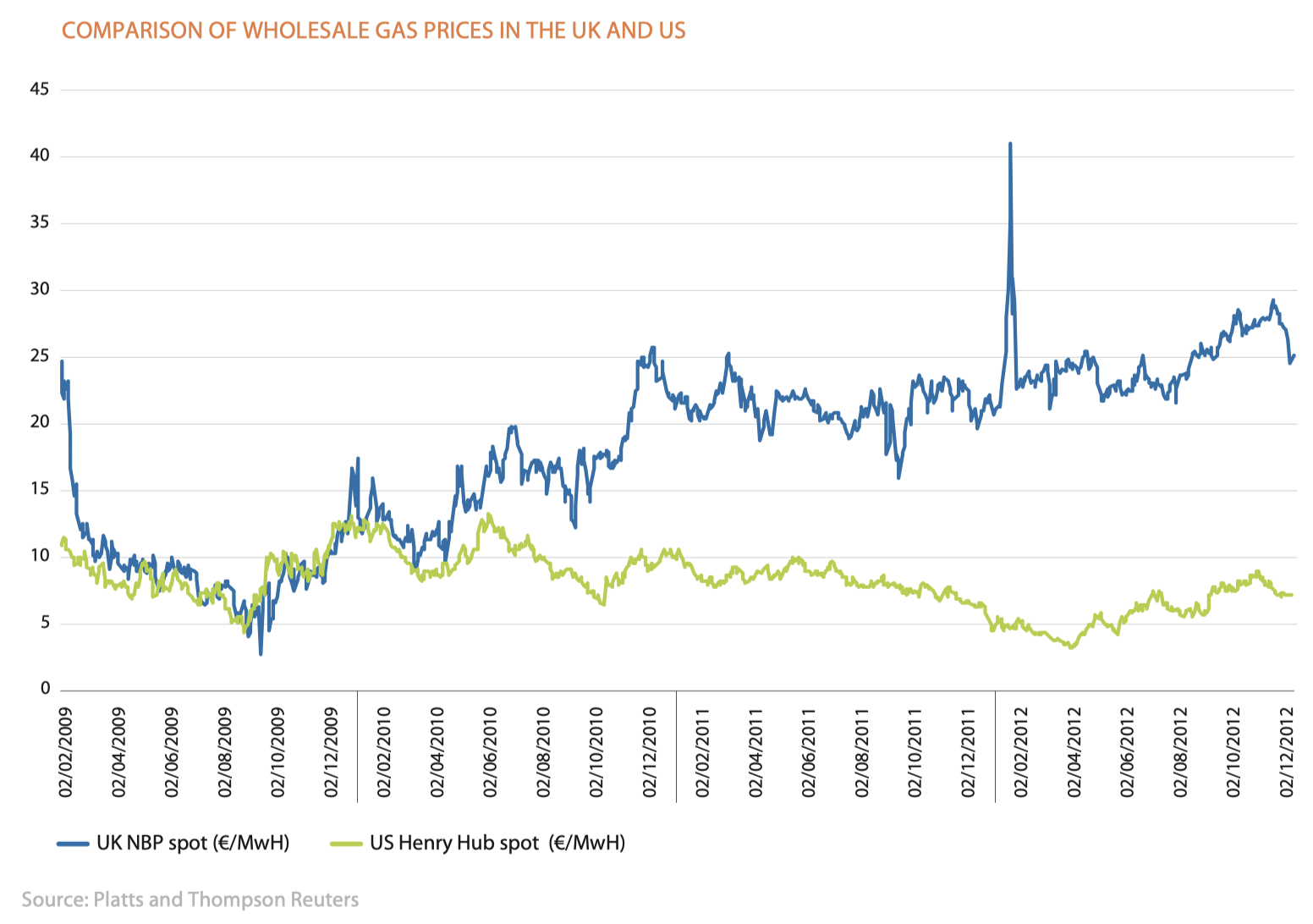

Gas prices in the European market rose by three times on average over the past 10 years whereas those of the US market varied upwards within 30%.

Meanwhile, according to the information of the European commission, the average UK NBP (spot) gas price did not exceed 25 EUR MWh over the past 4 years while the average price of LNG demonstrated growth from $7 up to $10.2 MMBtu at hubs of Great Britain, Spain, Italy, France, Belgium, Portugal and Greece.

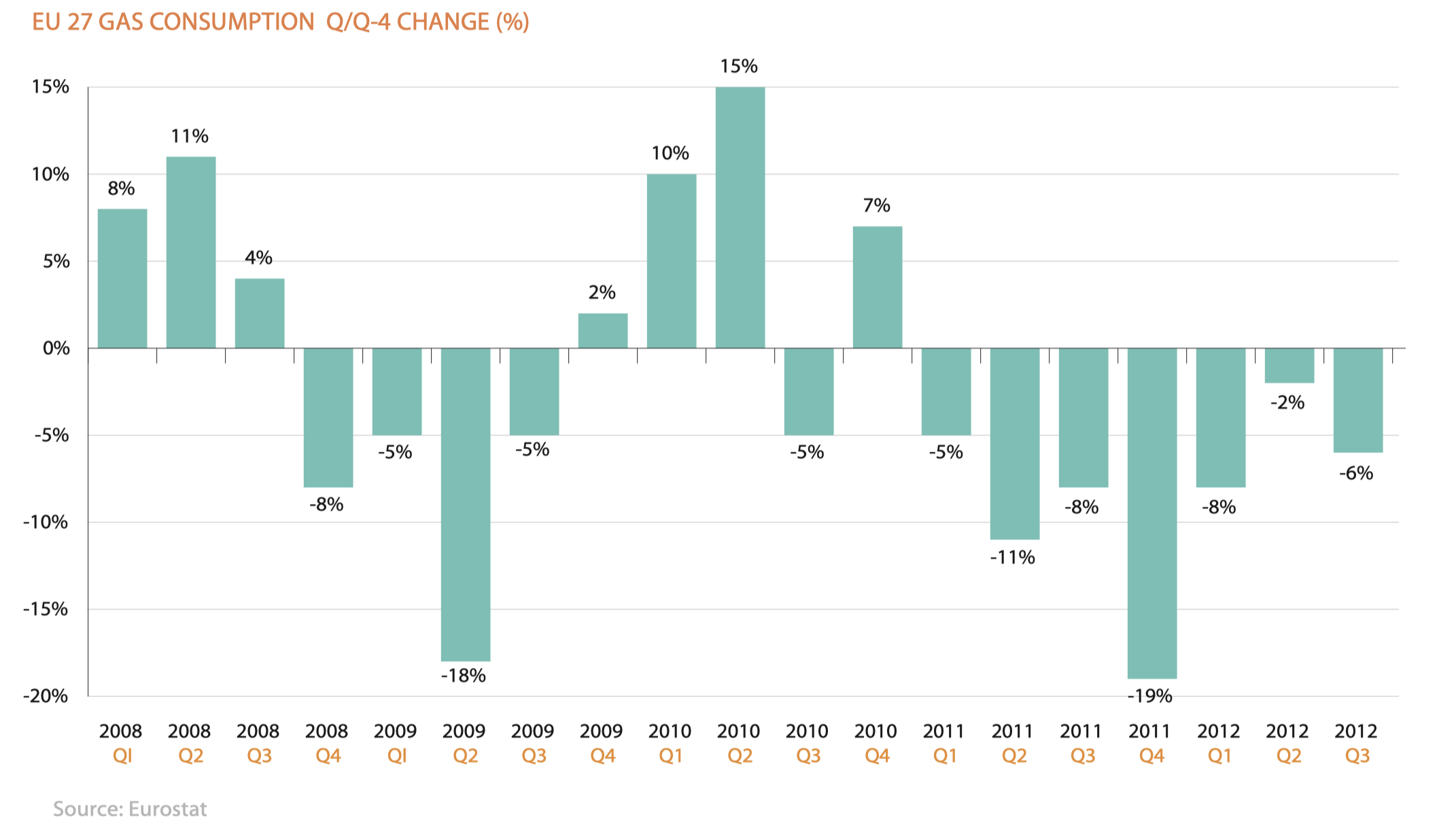

Since 2008 natural gas consumption in the EU has been demonstrating decline by -19% in 2011 and by -6% late in 2012.

The growth of coal consumption and switch of high-developed economies to renewable energy resources (60% of energy consumption of Denmark – the highest indicator in EU) was the response of the industrial economy of Europe to high prices for natural gas.

Shah Deniz gas is undoubtedly entering the big markets at a crucial moment when major trends for the long-term period have practically developed. However, as for the saying runs “The devil is in the detail”, so in this case it would be medium and short term risks of the world energy market as it is hard to clearly foresee and ignore them when it concerns price formation. It is the change of the export vector caused by the discovery of new reserves (USA, Mediterranean Sea, etc), emergence of new technologies (efficiency growth of renewable resources, production of shale resources), man-made cataclysms (Fukushima, BP’s accident in Gulf of Mexico, earthquakes near the Spanish coast where the nuclear power plant was located), different types of revolutions and combat operations or their threat in the energy sensitive regions (North Africa, Syria, Iran), climate change, appearance of new types of energy resources (methane hydrates, new bacteriological types of bio-fuel, kerogen shales and many others), strengthening of energy efficiency and environmental policy in the industrial countries. This list may be continued endlessly and it is not likely to reduce as time goes by. Therefore, the countries-producers have to be ready for that.

The present structure of the Shah Deniz shareholders is as following now: SOCAR (10%), BP (25.5%), Statoil (25.5%), LUKOIL (10%), NICO (10%), Total (10%) and TPAO (9%).

If we pay attention to the US energy market, it looks much safer and self-sufficient today. Apart from available natural resources, its three whales such as geographic isolation, stimulation of new exploration technologies and high rate of market liberalization may to some extent serve as a model of development for the Caspian regional market.

Anyway, more active development of the domestic market of gas and renewable resources, implementation of different areas-oriented joint regional projects together with other Caspian countries and the depth of penetration into different economic sectors will enable to maximally lower the influence of the above-mentioned risks over the long-term export energy policy of Azerbaijan.