")

")

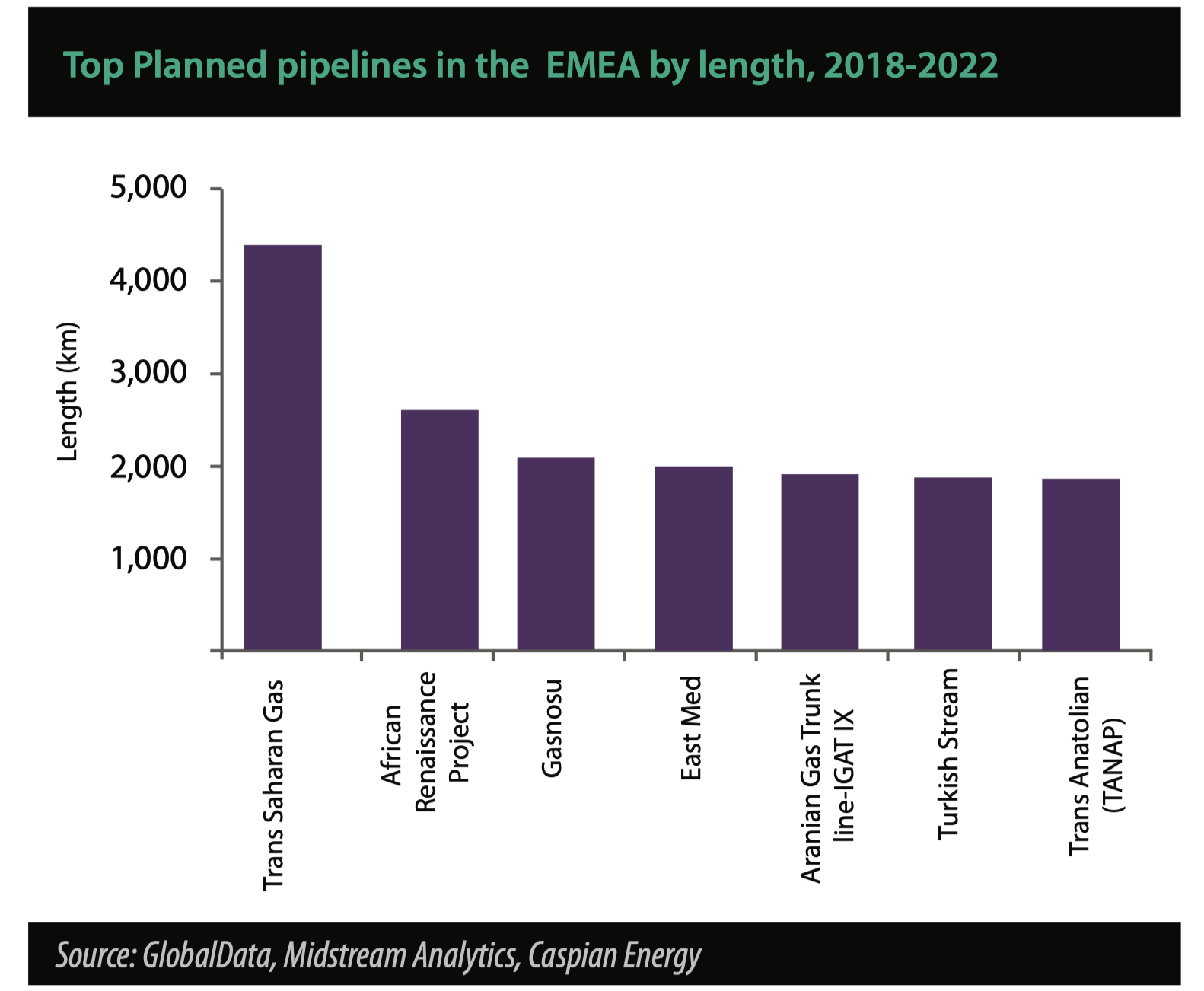

TANAP

The Trans-Anatolian Natural Gas Pipeline (TANAP) mega project, which is perhaps as important for the world energy market as the Baku-Tbilisi-Ceyhan system named after Heydar Aliyev, is nearing its completion. The gas pipeline through Georgia and Turkey will connect the Caspian gas fields with the European market. Officially, it will be put into operation on June 12, Minister of Energy and Natural Resources of Turkey Berat Albayrak said.

“There are no problems in the implementation of the TANAP project: Azerbaijan will be able to start gas exports to Turkey, and then to Europe. Turkey and the European countries will get access to a new alternative source”, President of the Republic of Azerbaijan Ilham Aliyev said.

The Contract of the Century-2 on the development of the Shah Deniz field was signed in Baku under the supervision of the National Leader of Azerbaijan Heydar Aliyev on June 4, 1996 and ratified by the Milli Majlis on October 17 of the same year. The participating interests in the Shah Deniz project are: BP (operator, 28.8%), Petronas (15.5%), SOCAR (16.7%), LUKOIL (10%), NICO (10%) and TPAO (19%). Gas production at the field began in December 2006.

The participating interests of the TANAP project are: SOCAR (51%), SOCAR Turkiye Enerji (7%), BOTAS (30%), and BP (12%).

The TANAP gas pipeline, along with the South Caucasus Pipeline and Trans Adriatic Pipeline (TAP), is a part of the Southern Gas Corridor (SGC) project which will enable gas transportation from the Caspian region to Europe.

Currently, gas production from the Shah Deniz field is carried out within the scope of Stage-1 worth $4.1 billion. Stage-1 envisages the output of 178 bcm of gas and 34 million tonnes of condensate.

The gas sales agreements were signed between Turkey, Azerbaijan and Georgia within the scope of Stage-1. The 690-km South Caucasus Pipeline (442 km in Azerbaijan and 248 km in Georgia) was built to enable export of Azerbaijani gas to Turkey.

In those days, low liquidity of natural gas, compared to oil, in the world markets and, as a result, the delayed financing of the European partners for the European section of the gas pipeline leads to the delay in the implementation of both Shah Deniz and SGC and only on September 19, 2013, agreements were signed with European gas buyers within the scope of the second stage of the Shah Deniz gas condensate field development in the Azerbaijani sector of the Caspian Sea.

Revenues under the gas supply contracts signed in Baku to transport about 300 bcm of Azerbaijan gas from the Shah Deniz field to Europe will comprise roughly $200 billion.

In particular, German E.ON will buy 40 bcm of Azerbaijan gas under the 25-year contract. Gas supplies will begin no earlier than 2019.

According to the statement of French GDF SUEZ, the company contracted 2.6 bcm of Azerbaijan gas per year.

Spanish Gas Natural Fenosa will receive 1 bcm of Azerbaijan gas annually, according to the company’s statement.

Italian company Hera will receive 300 million cubic metres of Azerbaijan gas per year within the scope of the concluded agreement.

In April 2018, the rights under the gas sales agreement under the Shah Deniz-2 project signed with the Spanish company Gas Natural Fenosa were transferred to the leading Italian energy company Edison.

In January 2018, TANAP General Manager Saltuk Duzyol said that over time other potential suppliers in Central Asia, the Middle East and the Eastern Mediterranean will also be able to access the market through this new route.

The groundbreaking ceremony of the TANAP gas pipeline was held on March 17, 2015 in Kars Province, Turkey. The throughput capacity of the pipeline will be at least 16 bcm, of which 10 bcm will be supplied to Europe, 6 bcm to the western regions of Turkey.

The project cost is estimated at $7.99 bln, while up to date expenditures on its implementation have exceeded $5.6 bln.

Forecasts

Noteworthy is that this time forecasts of the main players of the gas market are almost identical and sound in unison. They also coincide with the forecasts of CEOs of the oil and gas companies spoken during the World Energy Congress (Caspian Energy No.3 (101). This encourages strategic investors tired of instability in the world market in recent years. Reduced industry risks will secure an intensive growth of gas upstream projects, the LNG market, development of new production efficiency technologies, unbundling of gas quotes from the OPEC basket and benchmark crudes and, as a result, a growth of spot trading, creation of gas exchange sites of both regional and local importance.

Thus, the Gas Exporting Countries Forum (GECF) expects the gas demand to grow, and its share in the total energy basket by 2040 is expected to reach 26%, former Secretary General of the GECF Seyed Mohammed Hossein Adeli told reporters. “The gas demand will grow much faster than forecasted in previous years. And that’s good news. The share of gas in the total energy basket will grow to 26% by 2040. The share of gas in power generation will grow by 5% to reach 28%”, he said. The GECF will officially unveil its Global Gas Outlook until 2040 in November.

At that BP expects the global energy demand to grow by one third by 2040, runs BP’s traditional Energy Outlook-2018 unveiled on February 20, 2018.

The increase in global energy demand will be ensured by the rapid growth of emerging economies.

China and India will secure 50% of growth in energy demand by 2040, while Africa will be playing a bigger and bigger role closer to 2040.

At the same time today energy prices in China are traditionally higher than in the European market.

By 2040 the global energy mix will be the most diversified than ever.

The share of oil, gas, coal and non-fossil energy sources will amount to approximately 25% of the energy mix.

Renewable energy sources (RES) will grow most rapidly, showing a fivefold increase and securing about 14% of primary energy supplies.

The oil demand worldwide will grow up to 2040 and stabilize towards the end of the forecasted period.

The gas demand will grow faster and eventually will replace coal from the 2nd place among the largest energy sources.

By 2040, world supplies of liquefied natural gas (LNG) will grow more than twofold.

At the same time, already in early 2020s LNG supplies will exceed the volumes of inter-regional gas supplies via pipelines. At the same time, by 2040 the USA will account for almost 25% of global gas production and take the lead in this business.

Earlier, the US company Cheniere Energy Partners signed the 20-year contract for supply of 3.5 million tonnes of liquefied natural gas per annum to Korean Kogas. Gas is supplied from the third transfer line of the LNG plant at the Sabine Pass terminal in the Gulf of Mexico.

Earlier, Cheniere already signed contracts for 16 million tonnes a year from the annual total capacity of the four lines of the plant at 18 million tonnes. Other customers, besides Korea and India, are the companies of Spain (Fenosa), which owns the one third of 21 regasification terminals of the EU and the UK (BG).

Together, oil and gas will account for more than 50% of the world’s energy balance.

The electric power industry will account for almost 70% of an increase in demand for primary energy.

The balance of fuels used for power generation will change notably, while renewables will increase its share faster than any other type of fuel in history - from 7% to date to almost 25% by 2040.

Despite this, coal will keep the first place in power generation in 2040.

By 2040 carbon dioxide emissions will grow by 10%.

This is significantly lower than the growth rate of emissions over the past 25 years, but the growing trend is still expected to continue, rather than a significant decrease in emissions, which is necessary to achieve the goals of the Paris Agreement.

By 2040, the share of electric vehicles worldwide will grow to 15% of the entire fleet - more than 300 million cars out of almost 2 billion.

Competition

Unlike the USA, Europe does not have wide natural gas reserves to meet its domestic energy needs. Though, the European production (mainly in the North Sea via Norway and the Netherlands) is an important gas source for the continent. Its rates are rapidly falling as the old fields are diminishing. Meanwhile, the demand is growing and does not meet the rate set earlier (2% per year): according to the forecast of experts, by 2035 Europe will be in need of additional 120 bcm of imported gas.

Europe is now meeting over 50% of its gas demand through import. According to the latest official forecasts of the Norwegian agencies, gas production is planned to decline after 2020s. Gas production at Groningen, the biggest field of Europe, has decreased by more than half over the past 5 years. After the recent earthquakes, including the one which happened in January of this year, the Government of the Netherlands has made a decision about its decline down to 2 bln by 2030. If the gross consumption of energy resources in the EU drops 8% by 2050, the volume of gas consumption will rise by 6% compared to the figures of 2015 and constitute 25.4% of the energy balance. The renewable sector which is growing rapidly will have the same share. The major growth segments are transport, housing sector, and it is quite possible that it will involve the power industry if the EU is consistent with its ambition to reach the goals of the Paris agreement, which requires reduction of the coal share in generation.

Apart from this, the European legislation envisages consolidation and creation of new market zones. Thus, Quo Vadis has offered to develop 4 consolidated regional zones: 1) on the Iberian Peninsula; 2) the biggest one within Germany, Benelux, Czech Republic and Slovakia; 3) in the South-East Europe (Bulgaria, Romania); 4) in the Baltic countries.

Quo Vadis can be considered as an offered plan of actions (after 2018) for the next European Commission.

- Decline of growth rates of demand in the EU markets with a simultaneous growth of gas export volumes from new sources;

- Strengthening of the competition due to the implementation of the EU’s Third Energy Package conditions applicable to external supplies;

- Demand growth in China and India;

- Production increase in the Caspian;

All this suggests that there is a need to reform gas market architecture towards the active liberalization and creation of private upstream-oriented oil-gas companies, which will increase competitiveness of the gas industry in the global markets, draw investments into this sector and enable to build new interconnectors ensuring profitability of production and export of Caspian energy resources on the one hand, and secure a real long-term resource base for the SGC project on the other hand.

In addition to geopolitical and export dividends, implementation of TANAP and the entire Southern Gas Corridor can give an immense boost and lead to the development of the real competitive market of energy resources in the Caspian countries, create an exchange spot trade of energy resources, which, given the today’s market prospects and the experience gained by Azerbaijan while implementing Heydar Aliyev’s global oil-gas strategy for almost a quarter of a century, sounds real.